A Deep Dive into Digital Payments (Part 1)

A Deep Dive into Digital Payments (Part 1)

Take a peek behind the curtain to understand how the digital payments (via credit cards, debit cards, digital wallets) we make every day, online and offline, actually work and more.

If you aren’t subscribed, join your fellow curious and knowledge-addicted friends by subscribing here!

Hey friends 👋🏼

Writing this post brought on all sorts of imposter syndromes (i'm sure there's more than one cos I felt them all), especially since its a fairly technical topic. Unlike writing about engineering, 3D printing or Apple, I'm dipping my toe into a field I have neither the technical depth nor the work experience to write about with the nuance that it deserves.

However, from observing the world around me or from all the content I consume daily, sometimes I run into something interesting or even commonplace that I don't know enough about. That sometimes triggers a whole suite of questions in my mind about it. Not just on the surface but deep into the nuts and bolts. That makes it probably likely that many of you want to understand it a little better too. Hence, this is me learning and opining in public and like always, I am always happy to hear your feedback and constructive criticism.

Let's get it.

A Deep Dive into Digital Payments

(Note: Certain terms may be used interchangeably within the industry. Some of the concepts in this article have been simplified for readability)

The last 9 months have been a series of delivered meals, instacart-ed groceries and online purchases. When we go to the grocery store, we minimise contact, even with the cash in our wallets. Underlying these behavioural changes lies a single thread that enables us to continue these interactions seamlessly. Between you and Grubhub, you and the online store and even between you and your neighbourhood grocer. That thread is digital payments.

Before the pandemic struck, the industry was already projected to reach US$4.4 Trillion 🤯 in 2020 transaction volume. Now, this technology is more crucial then ever and we are using it more frequently than ever before. It has allowed us to access goods and services while in lockdown and limit in-person transactions. For merchants, the ease of onboarding onto these platforms have also helped many small businesses stay afloat.

For its critical role in our lives today, do we know how it works?

As a consumer, it's simple. We tap our cards/phones and wait for the approval "beep". Dig a little deeper however and you will find an array of processes that goes on behind the scenes, and an entire industry built around each step of processing every payment. Who's involved? How much are we paying? And who’s making money from this?

We'll find out answers to all these questions together. To get an understanding of digital payments and how it's evolving, we'll split this post into 2 parts to keep it somewhat human-readable. In this first post, we'll cover:

The credit card payments infrastructure. An in-depth understanding of how the payments infrastructure that processes most of our payments in the western world works. Who's involved, how does it flow and who gets paid?

Scale, Scale, Scale. The big players adapt to the changing demands of consumers and businesses.

A Closed loop Payments System. The holy grail for consumer +business facing payment firms.

In next week's post:

Emerging markets, one step ahead. The developing world + China have leapfrogged the western world and don't have to deal with the baggage of a legacy infrastructure. How does it work?

Peering into the future. I'll do my best impression of Elrond try glimpse how the payments space could look like in the next 5-10 years (for the uninitiated, that's a Lord of the Rings reference btw)

So many rabbit holes we can fall into when talking payments, but first...

The Credit Card Payments Infrastructure

As a consumer, it's so simple to make a digital payment. The ease of use and onboarding is what has contributed to such rapid adoption. But, as investors, developers, merchants or just curious folk (like us), we want a more detailed understanding of how the system works and who the key players are.

In most of the developed world, our digital payments system is built on top of the legacy credit card payments system. You might often hear that credit card payments run on what is often called a 4-Party network. But while it has 4 main parties, there are actually 7 key players involved.

The Key Players

Merchants

Stores; online or physical, where you make your purchases of goods or services from.

e.g: Amazon, Barnes & Noble, Your local grocery store.

Cardholder

You. The person making the payment and the owner of the credit/debit card.

Card Network

These are the rails that allows for the flow of transaction information and connects all the players in the network. The biggest players are household names whichever part of the world you hail from.

e.g: Mastercard, Visa, UnionPay, American Express

Payment Gateway

Gateways are the web-based equivalents of physical payment terminals. They ensure the secure authorisation and transfer of the customer's payment information to the processor. Usually for online or mail-order purchases only where the customer and card are not physically present at the store.

e.g: Paypal, Stripe, Square, Authorize.net

Payment Processor

The payment processor handles the technical side of processing the transactions. They provide the technology to pass along credit card information to the issuing bank, for movement of funds and sometimes, additional services like fraud detection and data analytics. While a payment processor is necessary to process the transaction, a payment processor alone doesn't help securely authorise the transaction.

e.g: Paypal, Square, MerchantOne, Flagship

Acquirer/Acquiring Bank

Acquiring bank are where merchants have their merchant accounts and store their funds. Acquiring banks work with independent payment processors. While the Payment Processors handle the technical aspects of the transaction, the liability and risk lie with the acquiring banks. Their risk departments are the ones that decide if merchants should be underwritten. This is because these banks are will be the ones receive the physical funds from the issuing bank.

e.g: Chase, Bank of America, DBS Bank, UOB Bank, Stripe, Adyen, WorldPay

Issuer/Issuing Bank

The financial institution (usually a bank) that issues credit (likely via a credit card) to consumers and provides the financial backing for transactions made on that credit.

e.g: Chase, Bank of America, DBS Bank, OCBC Bank, Discover

*Merchant Service Provider (MSPs)

Theses service providers refer companies that provide payment services to merchants and organisations that accept digital payments. These companies can be simply be a processor, a gateway or both. Which makes it a little confusing. Especially since the terms payment gateway, payment processor and merchant service provider are often used interchangeably. Most of the time, these MSPs, provide a whole suite of services under a clean, simple GUI. This abstracts away a lot of the complexity of the payments process and allows companies to very easily setup a payments system for their company.

e.g: Square, PayPal, Stripe

Now that we know the players, let’s dive into how they work together to keep trillions of dollars of payments flowing. Also, for consistent throughout our journey, I will be using the example of a consumer paying for a bag of chips at the grocery store whenever we talk about the payments flow.

The Process

Every time you make a digital payment, an entire array of players (mentioned above) are involved in authorising, clearing and settling that payment. The process, looks something like this:

*note that a fairly similar process also occurs for debit card payments.

Isn’t it amazing that this entire process, prior to settlement, happens in a matter of seconds 😮.

Who gets paid in this process?

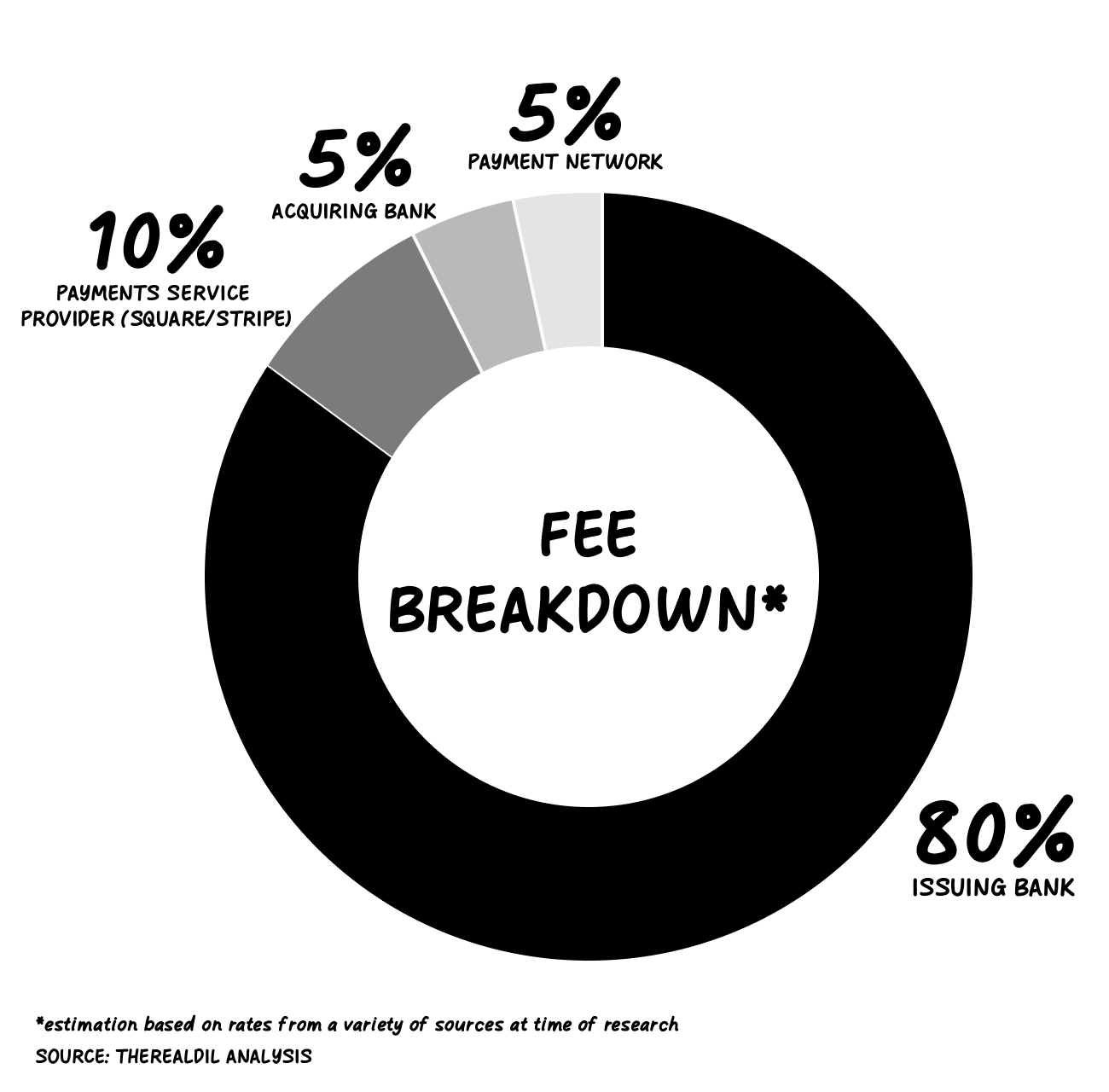

The $100 price that you see listed beside that new Bellroy bag you're planning to buy online is not entirely flowing into Bellroy's leather pockets. $2-$3 will be diverted to compensate the players for their role in the successful processing of a payment. The exact number varies depending on the card type, issuer, merchant service provider you're using (e.g square, dharma etc). This percentage also changes regularly so we won't be diving too deep into the details and will be using approximations.

These fees mainly comprise of 4 segments: Processing fees, Interchange fees, Scheme fees and the Acquirer Processing fee:

Processing Fee: This goes to the payments service provider (e.g Stripe) for facilitating the transaction.

Interchange Fee: This is paid to the issuing bank and accounts for the largest share of the fee breakdown. Since the issuing bank is the one who extends the line of credit to consumers and provides financial backing for transactions made on the card, it gets the largest reward. The fee is based on a complex structure and is usually set by the card networks.

Scheme Fee: This is paid to the various card schemes for use of their networks.

Acquirer Processing Fee: This is paid to the Acquirer/Acquiring Bank.

$2 out of a 100 may seem like a tiny amount. But once you realize that more than 110 million credit card transactions occur everyday just in the US, that $2 per 100 bucks really starts to add up.

Scale, Scale, Scale

While being a toll collector on the payments highway is probably one of the best business model's in the world, interchange and scheme fees have become subject to increasing scrutiny from regulators and merchant groups over the last decade. Networks and Banks are looking for alternative sources for revenue growth and margin preservation. Gateways and MSPs like Square are also in a cut throat business brawl, unable to increase fees despite margin pressure.

With the large consumer tech giants also bent on creating their own payment systems and grabbing a piece of the pie, it only adds to the margin pressure and competition in the space.

The conclusion that most of these payments companies have arrived at is that scale is the only way to survive. Considering the nature of the business where you're taking only a small fee from each transaction, to be successful you need sufficiently large transaction base. In addition, the number of payment options and complexity of systems have also increased the demand for more integrated solutions, especially for SMEs. Scale can come in different flavours:

Vertical or Geographical scale

Buy up competitors doing the same role in the value chain

Expand into new strategic markets, East to west or vice versa. (e.g PayPal's acquisition of the China based payment gateway, GoPay)

Horizontally across the Value Chain and Across payment modes

Own more functions along the value chain. (e.g Mastercard's acquisition of Vyze)

Own more input flows into the value chain (e.g Paypal’s acquisition iZettle)

We'll be paying more attention to the latter type in this post since expanding in terms of size and geography should be a simple concept to grasp.

Horizontal expansion is not a recent phenomenon. Many companies today already play a combination of multiple functions in the payments process. They come into the position either by one of three approaches:

Building the complementary capabilities in-house and receiving the appropriate licences.

Acquire independent players to strap-on capabilities that they do not have.

Form partnerships and wrap the multiple services under a unified "customer facing" platform so customers only deal with a single organisation to access multiple functions in the infrastructure.

By owning more of the value chain it allows companies to offer a more attractive proposition to merchants who now only have to integrate with a single, broader and more competitively priced platform. Secondly, these companies (depending on their config) also eliminate the need to siphon off fees to other players.

One example of this is Adyen. The company has spent the last decade on a mission to form a complete end to end solution. Already getting customers as an MSP offering gateway and processing solutions, it obtained a European acquiring license in 2012 to be able to offer acquiring services directly to its customers under its platform. The company also developed its own physical point of sale solution to increase transaction inflows via physical commerce. Today, Adyen also has banking licenses in several jurisdictions which allows it to settle payments on its own and possibly issue credit in the near future.

The graphic below illustrates the multiple roles being played by some of the largest and well known players in payments today (estimated and non-exhaustive).

As you can see, banks are becoming payment processors, card networks are acquiring payment gateways and payment gateway providers are issuing credit.

However, while owning the value chain is invaluable, companies with their own digital wallets, like Square and PayPal, have an even more lofty goal: A closed loop payments system.

The Holy Grail: A closed loop payments system

A ubiquitous two sided or closed loop network. This only occurs when both the merchant payments service provider and the customer's digital wallet are from the same company. This would disintermediate third parties (e.g card networks) and help to improve their transaction economics.

An example of a closed loop transaction: When someone spends with the Cash App at a Square merchant using Square's Cash for Business. These transactions are likely funded with Cash App users' balances and hence entirely processed within Square's own system. This means Square does not need to rely on external card networks or processors to communicate the transactions. The transactions are simply updated in Square’s digital ledger. For settlement of funds, while Square may not be the bank, since the transactions are occurring across its "clients" accounts in the same bank, an "on-us" transaction. The bank is able to process and authenticate the transaction internally (less fees!). This frees the company from having to bleed value to the networks on every transaction.

(on a side note: Square and PayPal have also obtained a banking licenses from the SEC)

It's impossible for any company to achieve a 100% closed loop as by default, that company would have to run the entire payment infrastructure. The goal for each company instead is to maximise the portion of the payments on the platform that is “closed-loop”. To succeed, they need to achieve sufficient network density on both the consumer and merchant sides.

With the parabolic user growth in digital wallets, Venmo (PayPal) and Cash App (Users), the 2 companies most well known to consumers have half the equation. This has led to much more focus on the merchant side. In this pursuit, PayPal, which has largely been focused on online and e-commerce transactions, has been on a mission to expand its transaction base by trying to penetrate the physical world. It acquired iZettle (a Square-like company in EU) in 2018 and now it has partnered with several major retailers including CVS to integrate Paypal's QR code technology at checkout. Square also already has an extensive QR code offering from being able to display one on their POS to QR codes for online checkout.

Both companies have also been looking to make their platforms more attractive to merchants/SMBs by broadening their suite of services (e.g.: lending, payroll, fraud detection etc)

To be clear, at this stage, the proportion of closed loop payments are probably still only a minuscule fraction of these companies total payment volumes. And unlike in other technology areas, in this space, the large US players are playing second fiddle to China, India and other emerging markets. Digital wallet payments only makes up about 2% of total transaction volumes in the US.

Before we go into the challenges specifically faced by US companies, we need to first understand the dynamics of how digital wallet payments work and how they have become so ubiquitous and successful in these other markets. That however, is a story for next week.

Don’t miss out on next week's post and more content like this:

Next week

In next week's post, we'll cover:

Emerging markets, A step ahead. The developing world + China have leapfrogged the western world and don't have to deal with the baggage of a legacy infrastructure. How does it work?

Peering into the future. I'll do my best impression of Elrond and try glimpse how the payments space could look like in the next 5-10 years (for the uninitiated, that's a Lord of the Rings reference btw)

Loved this! Has part 2 already come out?